Chapter 8: Selecting Corporate-Level Strategies

Diversification Strategies

Learning Objectives

- Explain the concept of diversification.

- Be able to apply the three tests for diversification.

- Distinguish related and unrelated diversification.

Firms using diversification strategies enter entirely new industries. While vertical integration involves a firm moving into a new part of a value chain that it is already within, diversification requires moving into an entirely new value chain. Many firms accomplish this through a merger or an acquisition, while others expand into new industries without the involvement of another firm.

Three Tests for Diversification

A proposed diversification move should pass three tests or it should be rejected (Porter, 1987).

- How attractive is the industry that a firm is considering entering? Unless the industry has strong profit potential, entering it may be very risky.

- How much will it cost to enter the industry? Executives need to be sure that their firm can recoup the expenses that it absorbs in order to diversify. The average drug developed by a major pharmaceutical company and approved by government costs at least $4 billion and as much as $11 billion.

- Will the new unit and the firm be better off? Unless one side or the other gains a competitive advantage, diversification should be avoided. In the case of developing new drugs, the costs may never be fully recovered.

Related Diversification

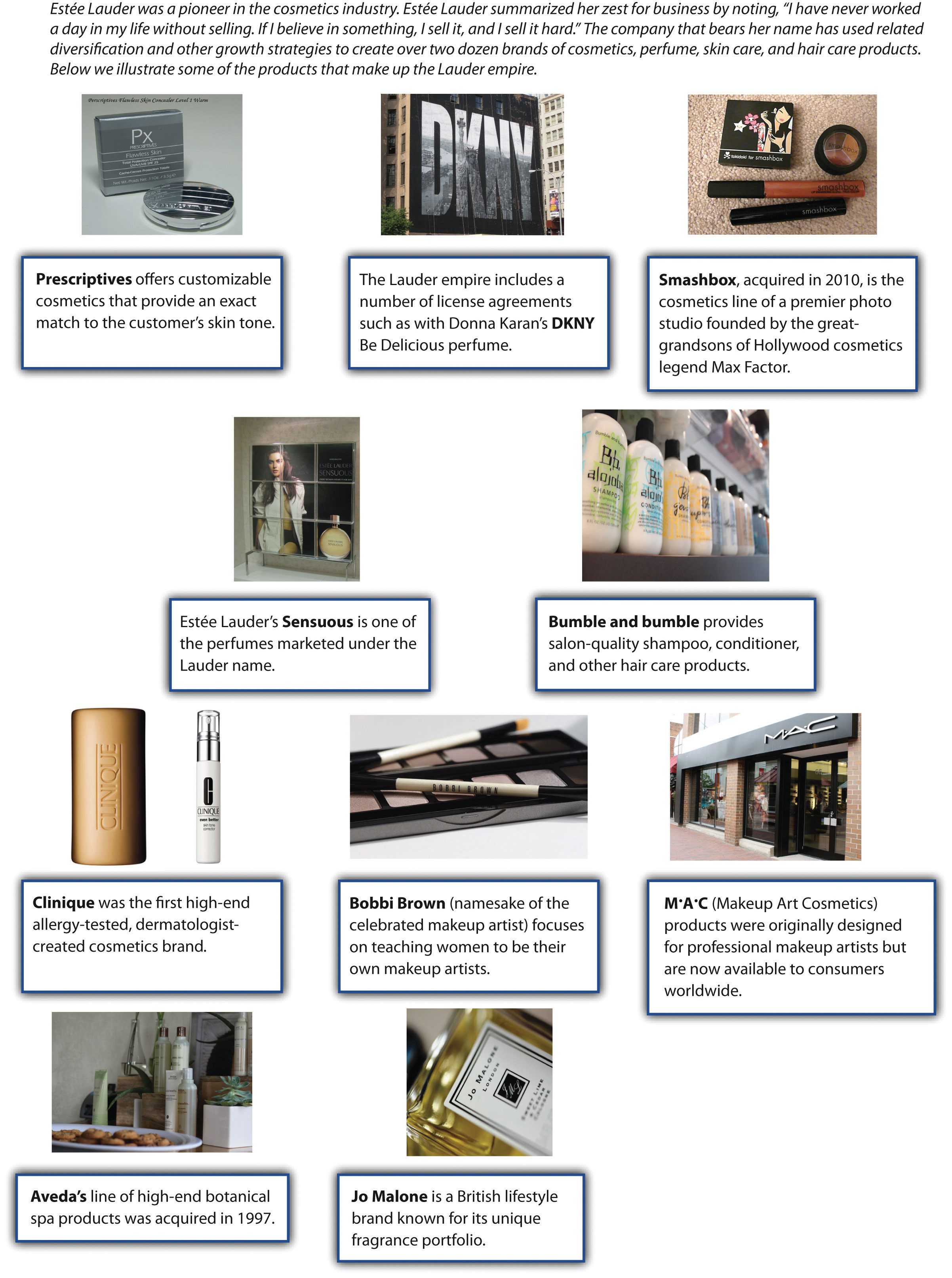

Related diversification occurs when a firm moves into a new industry that has important similarities with the firm’s existing industry or business lines (Figure 8.11 “The Sweet Fragrance of Success: The Brands That “Make Up” the Lauder Empire”). Since Google is in the information business, in 2014 it purchased Titan Aerospace, a maker of solar-powered drones, an example of related diversification. Some firms that engage in related diversification aim to develop and exploit a core competency to become more successful. A core competency is a skill set that is difficult for competitors to imitate, can be leveraged in different businesses, and contributes to the benefits enjoyed by customers within each business (Prahalad & Hamel, 1990). For example, Newell Rubbermaid is skilled at identifying underperforming brands and integrating them into their three business groups: (1) home and family, (2) office products, and (3) tools, hardware, and commercial products.

Honda Motor Company provides a good example of leveraging a core competency through related diversification. Although Honda is best known for its cars and trucks, the company actually started out in the motorcycle business. Through competing in this business, Honda developed a unique ability to build small and reliable engines. When executives decided to diversify into the automobile industry, Honda was successful in part because it leveraged this ability within its new business. Honda also applied its engine-building skills in the all-terrain vehicle, lawn mower, and boat motor industries. Most recently, Honda has developed an energy-efficient six-passenger HA-420 HondaJet aircraft, which is undergoing FAA approval.

Sometimes the benefits of related diversification that executives hope to enjoy are never achieved. Estée Lauder used to distribute Sean John Fragrance, but divested itself of the product line. Of course, Sean John is P. Diddy, among other aliases. He still continues to sell fragrances, the latest called, I Am King.

Unrelated Diversification

Why would a soft-drink company buy a movie studio? It’s hard to imagine the logic behind such a move, but Coca-Cola did just this when it purchased Columbia Pictures in 1982 for $750 million. This is a good example of unrelated diversification, which occurs when a firm enters an industry that lacks any important similarities with the firm’s existing industry or industries (Figure 8.13 “Unrelated Diversification at Berkshire Hathaway”). Luckily for Coca-Cola, its investment paid off—Columbia was sold to Sony for $3.4 billion just seven years later.

Most unrelated diversification efforts, however, do not have happy endings. Harley-Davidson, for example, once tried to sell Harley-branded bottled water. Starbucks tried to diversify into offering Starbucks-branded furniture. Such initiatives are very expensive, both in direct costs such as marketing and indirect costs such as executive time. However, these efforts were disasters. Although Harley-Davidson and Starbucks both enjoy iconic brands, these strategic resources simply did not transfer effectively to the bottled water and furniture businesses.

Lighter firm Zippo is currently trying to avoid this scenario. According to CEO Geoffrey Booth, the Zippo is viewed by consumers as a “rugged, durable, made in America, iconic” brand (AP News, 2011). This brand has fueled eighty years of success for the firm. But with fewer smokers, the future of the lighter business is bleak. Zippo executives expect to sell about 12 million lighters this year, which is a 50 percent decline from Zippo’s sales levels in the 1990s. This downward trend is likely to continue as smoking becomes less and less attractive in many countries. To save their company, Zippo executives want to diversify.

In particular, Zippo wants to follow a path blazed by Eddie Bauer and Victorinox Swiss Army Brands Inc. The rugged outdoors image of Eddie Bauer’s clothing brand has been used effectively to sell sport utility vehicles made by Ford. The high-quality image of Swiss Army knives has been used to sell Swiss Army–branded luggage and watches. As of March 2011, Zippo was examining a wide variety of markets where their brand could be leveraged, including watches, clothing, wallets, pens, liquor flasks, outdoor hand warmers, playing cards, gas grills, and cologne. Trying to figure out which of these diversification options could be winners, such as the Eddie Bauer-edition Ford Explorer, and which would be losers, such as Harley-branded bottled water, is a key challenge facing Zippo executives.

Strategy at the Movies

In Good Company

What do Techline cell phones, Sports America magazine, and Crispity Crunch cereals have in common? Not much, but that did not stop Globodyne from buying each of these companies in its quest for synergy in the 2004 movie In Good Company. Executive Carter Duryea was excited when his employer Globodyne purchased Waterman Publishing, the owner of Sports America magazine. The acquisition landed him a big promotion and increased his salary to “Porsche-leasing” size.

Synergy is created when two or more businesses produce benefits together that could not be produced separately. While Duryea was confident that a cross-promotional strategy between his advertising division and the other units within the Globodyne universe was a slam-dunk, Waterman employee Dan Foreman saw little congruence between advertisements in Sports America on the one hand and cell phones and breakfast cereals on the other. Despite his considerable efforts, Duryea was unable to increase ad pages in Sports America because the unrelated nature of Globodyne’s other business units inhibited his strategy of creating synergy. Seeing little value in owning a failing publishing company, Globodyne promptly sold the division to another conglomerate. After the sale, the executives that had been rewarded for the initial purchase of Waterman Publishing, including Duryea, were fired.

Globodyne’s inability to successfully manage Waterman Publishing illustrates the difficulties associated with unrelated diversification. While buying companies outside a parent company’s core competencies can increase the size of the company and in turn its executives’ bank accounts, managing firms unfamiliar to management is generally a risky and losing proposition. Decades of research on strategic management suggest that when firms diversify, it is best to “stick to the knitting.” That is, stay with businesses executives are familiar with and avoid moving into ventures where little expertise exists.

Key Takeaways

- Diversification strategies involve firmly stepping beyond its existing industries and entering a new value chain. Generally, related diversification (entering a new industry that has important similarities with a firm’s existing industries) is wiser than unrelated diversification (entering a new industry that lacks such similarities).

Exercises

- Studies have shown that executives’ pay increases when their firms gets larger. What role, if any, do you think executive pay plays in diversification decisions?

- Identify a firm that has recently engaged in diversification. Search the firm’s website to identify executives’ rationale for diversifying. Do you find the reasoning to be convincing? Why or why not?

References

AP News. (2011). Zippo’s burning ambition lies in retail expansion. Townhall.com. Retrieved from http://th2010.townhall.com/news/us/2011/03/20/zippos_burning_ambition_lies_in_ retail_expansion.

Herper, M. (2012, February 10). The Truly Staggering Cost Of Inventing New Drugs, Forbes. Retrieved from http://www.forbes.com/sites/matthewherper/2012/02/10/the-truly-staggering-cost-of-inventing-new-drugs/

Mack, E. (2014, April 14). Google Confirms Purchase Of Titan Aerospace For Data Drone Effort, Forbes. Retrieved from http://www.forbes.com/sites/ericmack/2014/04/14/google-reportedly-buying-solar-drone-maker-not-facebook/

Porter, M. E. (1987). From competitive advantage to corporate strategy. Harvard Business Review, 65(3), 102–121.

Prahalad, C. K., & Hamel, G. (1990). The core competencies of the corporation. Harvard Business Review, 86(1), 79–91.

Wikipedia Organization. (2014). HA-420 HondaJet. Retrieved from http://en.wikipedia.org/wiki/Honda_HA-420_HondaJet

Image description

Figure 8.11 image description: The Sweet Fragrance of Success: The Brands That “Make Up” the Lauder Empire

Estée Louder MS pioneer in the cosmetic industry Estée Lauder summarized her zest for business by noting “I have never worked a day in my life without selling. If I believe in something, I sell it and I sell it hard.” and it The Company bears her name has used related diversification and other growth strategy to create over two dozen brands of cosmetics, perfume. Skin Care and hair care products. Below we illustrate some of the products that make up the Lauder empire.

- Prescriptives offers customizable cosmetics that provide an exact match to the customers skin tone.

- The lauder empire a number of license agreements such as with Donna DKNY Be Delicious perfume.

- Smashbox, acquired in 2010, is the cosmetics line of a photo studio founded by the great-grandsons of cosmetics legend Max Factor.

- Estée Lauder Sensuous is on of the perfumes marketed under the Lauder name.

- Bumble and bumble provides salon-quality shampoo, conditioner, and other hair care products.

- Clinique was the first high-end allergy-tested, dermatologist-created cosmetics brand.

- Bobbi Brown (namesake of the celebrated makeup artist) focus on teaching women to be their own makeup artists.

- MAC (Makeup Art Cosmetics) products originally designed for professional makeup artists but are now available to consumers worldwide.

- Aveda’s line Of high-end botanical spa products was acquired in 1997.

- Jo Malone is a British lifestyle brand know for its unique fragrance portfolio.

Figure 8.13 image description: Unrelated Diversification at Berkshire Hathaway

“Don’t put your eggs in one basket” is often a good motto for individual investors. By building a portfolio of stocks, an investor can minimize the chances of suffering a huge loss. Some executives take a similar approach. Rather than trying to develop synergy across businesses, they seek greater financial stability for their firms by owning on array of compomes. Warren Buffett’s Berkshire Hathaway has Jong enjoyed strong performance by purchasing companies and improving how they Ore run. Below we illustrate some of the different groups in their very diversified portfolio of firms.

- Berkshires insurance group includes firms such as General Re and GEICO They maintain capital strength at exceptionally high levels, which gives them an advantage even a cave man could understand.

- Berkshire’s financial health is also fueled by utilities and energy companies that are part of the MidAmerican Energy Holdings Company.

- Their apparel businesses include well-known names such Fruit of the Loom and Justin Brands.

- Building companies include Acme Building Brands, makes Of the famous brick, as well as paint company Benjamin Moore & Co.

- FlightSafety International Inc. is a Berkshire firm that engages in high-tech training to aircraft and ship operators.

- Retail holdings include a number of furniture businesses such as R.C. Willey Home Furnishings, Star Furniture Company, and Jordan’ Furniture. Inc.

- Hungry for more businesses to manage, Berkshire acquired The Pampered Chef, Ltd.—the largest direct kitchen tools seller—in 2002.

- Buffett had a sweet tooth for See’s Candies, who he purchased from the See’s family in 1972.

- Shareholders were all on board for the purchase of the Burlington Northern Santa Fe Corporation in 2009.

Involve a firm entering entirely new industries.

When a firm moves into a new industry that has important similarities with the firm’s existing industry or industries.

A skill set that is difficult for competitors to imitate, can be leveraged in different businesses, and contributes to the benefits enjoyed by customers within each business.

When a firm enters an industry that lacks any important similarities with the firm’s existing industry or industries.